When you sell or exchange real estate, there’s more to the deal than just signing the paperwork and collecting your proceeds. Behind the scenes, the IRS requires certain parties to report these transactions using Form 1099-S, which captures the sale details for tax compliance. Whether you’re a title company, attorney, or seller involved in a property transfer, understanding how Form 1099-S works is crucial to avoiding penalties and ensuring accurate tax reporting. This guide will walk you through who must file it, key deadlines, how to complete and file the form, exemptions, penalties, and what sellers should do upon receiving one.

What Is Form 1099-S?

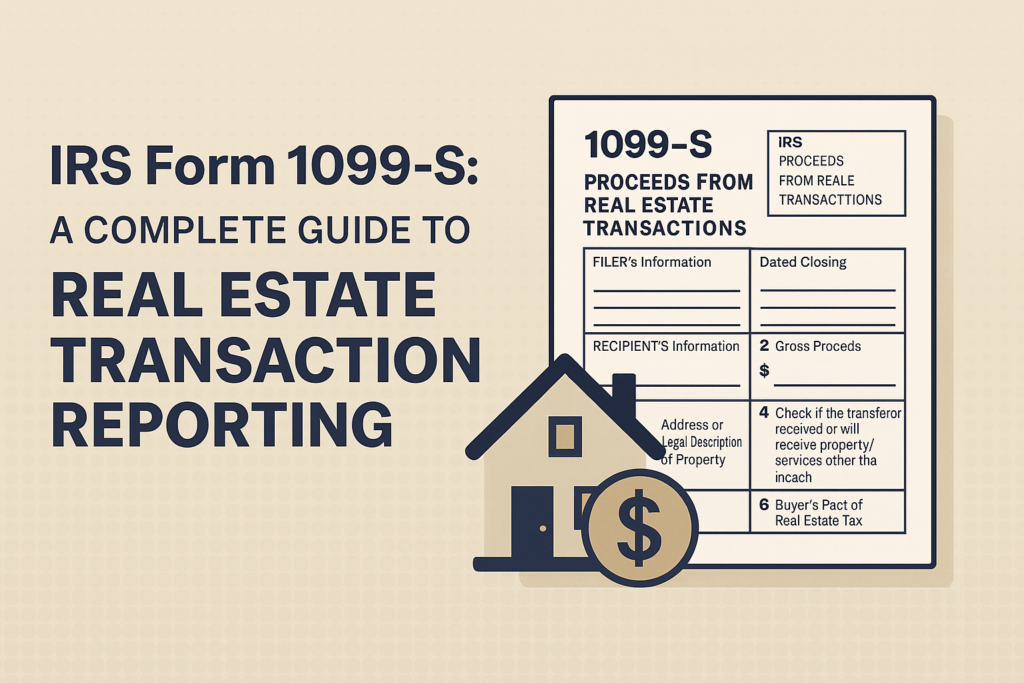

Form 1099-S, Proceeds from Real Estate Transactions, is an IRS information return used to report the sale or exchange of real estate. It helps the IRS ensure taxpayers properly report gains or losses from property transactions on their tax returns.

This form is typically used for transactions involving land, residential homes, commercial buildings, and even partial interests in property. When a sale or exchange takes place, the party responsible for closing the transaction—often a title company, attorney, or escrow agent—must file Form 1099-S with the IRS and furnish a copy to the seller.

Who Must File Form 1099-S?

The responsibility to file Form 1099-S lies with the person or entity that conducts the closing of a real estate transaction. This could be a:

- Real estate attorney

- Settlement or escrow agent

- Title company

- Mortgage lender

- Real estate broker

If no such person is designated, the responsibility may fall to the mortgage lender or the seller’s agent.

Real-Time Examples:

- Example 1: A title company finalizes the closing of a house sale in California. Since they conducted the closing, they must file Form 1099-S to report the sale proceeds to the IRS and send a copy to the seller.

- Example 2: A real estate attorney in Florida handles the settlement of a commercial property transaction. They are responsible for completing and filing Form 1099-S.

- Example 3: A private seller in Texas sells a piece of farmland without using a title agent or attorney. If no closing agent is involved, the obligation to file may fall back to the seller.

When Is the Deadline to File Form 1099-S?

There are two key deadlines associated with Form 1099-S:

- Recipient Copy Deadline:

Must be furnished to the seller by January 31 of the year following the sale. - IRS Filing Deadlines:

- Paper filing: Due by February 28

- Electronic filing: Due by March 31

- Missing these deadlines can result in penalties, so it’s crucial to plan ahead.

What Information is Required to Complete Form 1099-S?

To accurately complete Form 1099-S, the following information is needed:

- Name, address, and TIN (Taxpayer Identification Number) of the seller

- Date of closing

- Gross proceeds from the sale

- Property description (legal or otherwise)

- Buyer’s name and TIN (if applicable)

- Whether the seller is a foreign person

- Any exemption certifications (like principal residence)

This information is typically collected during closing using Form W-9 and other disclosure documents.

How to Complete Form 1099-S?

Here is a breakdown of each section and box on Form 1099-S:

FILER’S Information

- Name, address, phone number, and TIN of the entity filing the form (e.g., title company).

RECIPIENT’S Information

- Name, address, and TIN of the seller.

Box 1 – Date of Closing

- Enter the date when the sale or exchange of the property was finalized.

Box 2 – Gross Proceeds

- Report the total amount received from the transaction. Do not subtract fees, commissions, or other costs.

Box 3 – Address or Legal Description of Property

- Provide the physical address of the property or legal description if no address exists (e.g., vacant land).

Box 4 – Check if the transferor received or will receive property/services other than cash

- If applicable, check this box to indicate that part of the consideration was not cash (e.g., barter or exchange).

Box 5 – Check if the transferor is a foreign person

- If the seller is a non-U.S. person, this box should be checked. This may trigger additional tax rules under FIRPTA (Foreign Investment in Real Property Tax Act).

Box 6 – Buyer’s Part of Real Estate Tax

- Report any portion of the real estate taxes paid by the buyer, if the information is known.

How to File Form 1099-S?

There are two methods to file Form 1099-S with the IRS:

1. Paper Filing

- Use Form 1096 as a cover sheet.

- Mail to the IRS address listed in the form instructions based on your location.

2. Electronic Filing (E-File)

- Required if submitting 250 or more forms, but allowed for fewer.

- Use the FIRE system (Filing Information Returns Electronically) provided by the IRS.

- Requires registration and a TCC (Transmitter Control Code).

Additionally, a copy of Form 1099-S must be provided to the seller by the January 31 deadline.

What Are the Penalties for Not Filing Form 1099-S?

Failure to file or furnish Form 1099-S may result in the following penalties:

| Delay | Penalty per Form | Maximum Annual Penalty (Small Business) |

| ≤30 days late | $60 | $220,500 |

| 31 days to Aug 1 | $120 | $630,500 |

| After Aug 1 or not filed | $310 | $1,261,000 |

| Intentional Disregard | $630+ | No Limit |

Penalties can double if both the IRS filing and recipient copy are not furnished.

How to Extend 1099-S Filing and Recipient Copy Deadline?

You can request an extension by using the following methods:

For IRS Filing:

- Use Form 8809 (Application for Extension of Time to File Information Returns) to request an automatic 30-day extension.

- Must be filed by the original due date (Feb 28 for paper, Mar 31 for electronic).

For Recipient Copy:

- Use Form 15397 (Request for Extension of Time to Furnish Statements to Recipients) to apply for a 30-day extension for providing seller copies.

- A written explanation is required to justify the extension.

Who Is Exempt from Filing Form 1099-S?

Some real estate transactions are exempt from 1099-S reporting. These include:

- Sale of a principal residence where the gain is excluded under IRS rules (up to $250,000 for single filers or $500,000 for joint filers) and the seller certifies the exemption.

- Certain corporate transfers

- Tax-exempt organizations acquiring the property

- Foreclosures and certain mortgage lender repossessions

- Gifts or property transfers due to inheritance

Exemption documentation (such as a signed certification from the seller) must be retained by the filer.

What Should Recipients Do With Form 1099-S?

As a recipient (seller), you should:

- Review the Form:

Confirm the accuracy of the sale amount, closing date, and property description. - Report the Transaction on Your Tax Return:

Even if you qualify for a gain exclusion on your primary residence, you still need to report the sale on Schedule D and Form 8949 of your federal return.

Keep for Your Records:

The form acts as proof of sale and IRS-reported income, so keep it for future reference.

Final Thoughts

Form 1099-S plays a vital role in ensuring transparency in real estate transactions. Whether you’re a title company, real estate attorney, or private seller, understanding your responsibilities can help avoid costly penalties. Meanwhile, recipients must report proceeds properly to avoid audit issues. Knowing the deadlines, exemptions, and filing steps ensures a smoother process for all parties involved.