If you’ve ever withdrawn money from a Health Savings Account (HSA), Archer Medical Savings Account (MSA), or Medicare Advantage MSA, you may have come across IRS Form 1099-SA in your mailbox. This form is the IRS’s way of keeping tabs on distributions from these tax-advantaged accounts, ensuring that funds were used for qualified medical expenses—or taxing them if they weren’t.

For account custodians (such as banks, credit unions, or insurance companies), Form 1099-SA isn’t just a courtesy—it’s a mandatory IRS filing requirement. For recipients, it’s an important piece of tax documentation that can affect whether you owe taxes or penalties.

This guide breaks down everything you need to know—from who files the form, what it reports, how to complete it line by line, filing deadlines, penalties, exceptions, and how it differs from Form 5498-SA.

What Is Form 1099-SA?

Form 1099-SA is an IRS information return used to report distributions from:

- HSAs – Health Savings Accounts

- Archer MSAs – Archer Medical Savings Accounts

- Medicare Advantage MSAs – A type of medical savings account for Medicare enrollees

It is issued by the account trustee or custodian when a withdrawal, transfer, or distribution occurs. The form tells both you and the IRS:

- The total amount withdrawn

- Whether the withdrawal was for qualified medical expenses

- Any taxable portion and penalties

Purpose: To ensure tax compliance and track whether distributions remain tax-free or are subject to income tax and penalties.

Who Can File Form 1099-SA?

The responsibility to file Form 1099-SA falls on the trustee or custodian of the account—not the account holder.

Typical filers include:

- Banks and credit unions managing HSAs/MSAs

- Insurance companies offering MSA-linked products

- Medicare Advantage MSA administrators

If multiple distributions occur in a year, only one form per account is generally filed unless different distribution codes apply, in which case separate forms may be required.

Who Receives Form 1099-SA?

The recipient copy is sent to:

- The account holder (the person whose name is on the HSA or MSA)

- In the case of inherited accounts, the beneficiary receiving the funds

The IRS also gets its own copy to cross-check with the tax return you file.

Tax-Free Distributions

Distributions from an HSA, Archer MSA, or Medicare Advantage MSA are tax-free if:

- Used to pay for qualified medical expenses (as defined in IRS Publication 502)

- The expenses were incurred after the HSA/MSA was established

- Documentation of the expenses is kept for records

Example: You withdraw $3,000 from your HSA to pay for surgery. As long as the expense was qualified and properly documented, it’s not taxable.

Taxable Distributions

A distribution becomes taxable if:

- It’s used for non-qualified expenses

- You can’t prove the expense was qualified during an IRS audit

- You received funds before meeting eligibility requirements (e.g., non-medical withdrawal before age 65 from an HSA)

Tax effect:

- The amount is added to your taxable income

- An additional 20% penalty usually applies to HSAs and Archer MSAs (penalty waived for disability, death, or age 65+)

Inherited Accounts and Taxes

When an HSA or MSA is inherited:

- If the beneficiary is a spouse, the account remains an HSA/MSA and retains its tax benefits.

- If the beneficiary is a non-spouse, the account ceases to be an HSA/MSA, and the entire fair market value becomes taxable income in the year of death.

When Is the Deadline to File Form 1099-SA?

Key deadlines for the 2025 tax year:

- Recipient Copy Distribution: January 31, 2026

- Paper Filing with IRS: February 28, 2026

- E-File with IRS: March 31, 2026

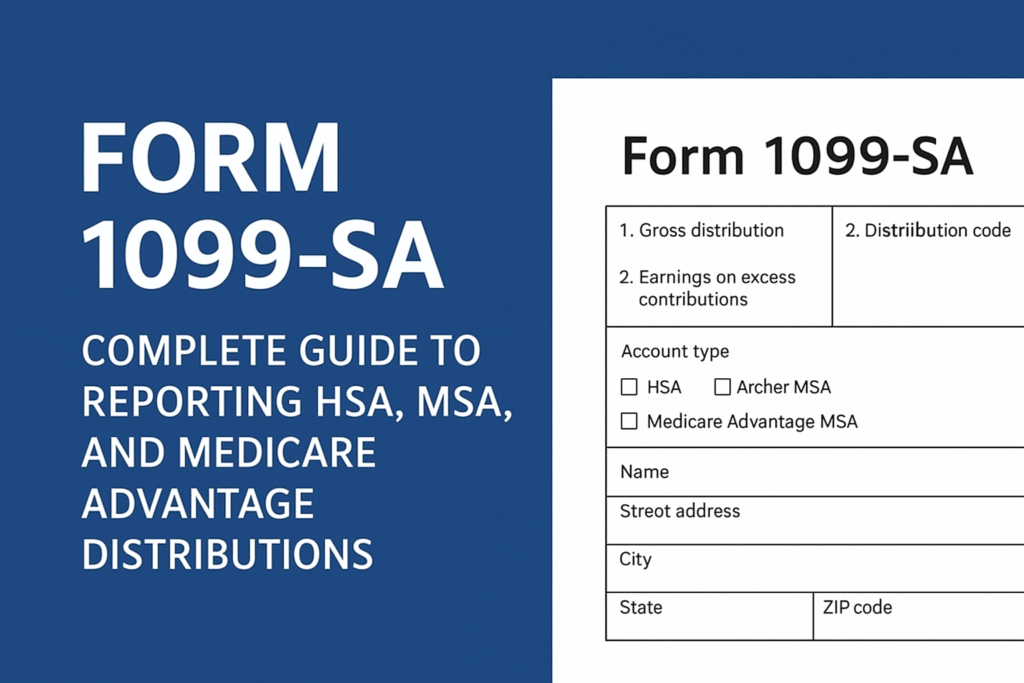

What Information Is Required to Complete Form 1099-SA?

To prepare the form, custodians need:

- Account holder’s name, address, and SSN

- Trustee’s/custodian’s name, address, and TIN

- Total distribution amount

- Earnings on excess contributions (if applicable)

- Distribution code (explains the reason for withdrawal)

- Account type (HSA, Archer MSA, Medicare Advantage MSA)

How to Complete Form 1099-SA – Line by Line Instructions

Basic Information

Payer’s name, address, TIN: Fill in completely; payer’s TIN must not be truncated.

Recipient’s TIN, name, address: Input as provided. Recipient’s TIN may be truncated for privacy on Copy B, but never on Copy A.

Account Number: Required if filing multiple forms for one recipient; encouraged for all forms.

Information on Distributions

Box 1 – Gross Distribution

Enter the total amount distributed from the account during the year, including direct payments to medical providers.

Box 2 – Earnings on Excess Contributions

Report any earnings attributable to excess contributions withdrawn.

Box 3 – Distribution Code

Enter the correct code:

- 1 – Normal distribution

- 2 – Excess contributions plus earnings taxable in current year

- 3 – Disability

- 4 – Death distribution other than code 6

- 5 – Prohibited transaction

- 6 – Death distribution after death of account holder to a non-spouse beneficiary

Box 4 – FMV on Date of Death

If applicable, enter the account’s fair market value on the date of death.

Box 5 – Account Type

Check the correct box: HSA, Archer MSA, or Medicare Advantage MSA.

What Are the Copies in Form 1099-SA?

Form 1099-SA is issued in multiple copies, each serving a distinct purpose for the IRS, the recipient, and the filer.

- Copy A – Sent to IRS

- Copy B – Sent to the recipient (taxpayer)

- Copy C – Retained by the filer for records

How to File Form 1099-SA?

Filing Form 1099-SA involves sending the required copies to both the IRS and the account holder to report distributions from certain medical savings accounts. The process can be done electronically or by mail, but it must follow IRS rules and deadlines to ensure accuracy and avoid penalties.

- Electronic filing is encouraged if filing 10 or more information returns. Use IRS FIRE System for e-filing

- Paper filing requires Form 1096 transmittal

Where to Mail Form 1099-SA

If paper filing, mail to the correct IRS address for your state

| If your business operates in or your legal residence is | Mail Form 1099-SA to |

| Alabama, Arizona, Arkansas, Delaware, Florida, Georgia, Kentucky, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Texas, Vermont, Virginia | Internal Revenue ServiceAustin Submission Processing Center P.O. Box 149213 Austin, TX 78714 |

| Alaska, Colorado, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Montana, Nebraska, Nevada, North Dakota, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Utah, Washington, Wisconsin, Wyoming | Department of the TreasuryIRS Submission Processing Center P.O. Box 219256 Kansas City, MO 64121-9256 |

| California, Connecticut, District of Columbia, Louisiana, Maryland, Pennsylvania, Rhode Island, West Virginia | Department of the TreasuryIRS Submission Processing Center1973 North Rulon White Blvd. Ogden, UT 84201 |

Penalties for Not Filing Form 1099-SA

Penalties apply if you:

- Fail to file by the deadline

- File with incorrect information

- Fail to furnish the recipient copy

Penalty amounts (2025):

- $60 per return (if filed within 30 days of due date)

- $120 per return (if filed after 30 days but before August 1)

- $310 per return (if filed after August 1 or not filed at all)

How to Extend the 1099-SA Deadline

If you are a filer responsible for issuing Form 1099-SA, you must meet strict IRS deadlines for both furnishing copies to recipients and submitting the form to the IRS. However, in certain circumstances, you can request an extension to avoid late-filing penalties.

There are two main ways to request extra time, depending on which deadline you are trying to extend — Form 8809 for IRS filing and Form 15397 for recipient copy extensions.

Exceptions to Filing Form 1099-SA

While Form 1099-SA is generally required whenever there is a distribution from a Health Savings Account (HSA), Archer Medical Savings Account (Archer MSA), or Medicare Advantage MSA, the IRS provides certain exceptions where filing the form is not necessary. Understanding these exceptions helps filers avoid unnecessary paperwork and focus only on reportable distributions.

| Situation | 1099-QA Filing Required? | Reason |

| No distribution during the year | ❌ No | No funds withdrawn |

| Trustee-to-trustee transfer | ❌ No | Direct transfer is not a distribution |

| Rollover within 60 days | ❌ No | Treated as non-taxable rollover |

| Corrected form replaces mistaken filing | ❌ No | Duplicate reporting not needed |

| Already reported on another IRS form | ❌ No | Reporting requirement already met |

| Non-distribution transactions | ❌ No | Not a reportable event |

Difference Between Form 1099-SA and Form 5498-SA

Although Form 1099-SA and Form 5498-SA are both related to Health Savings Accounts (HSAs), Archer Medical Savings Accounts (Archer MSAs), and Medicare Advantage MSAs (MA MSAs), they serve entirely different reporting purposes. Understanding the difference between these two forms is essential for both account holders and trustees or custodians to ensure accurate tax reporting and compliance.

| Feature | Form 1099-SA | Form 5498-SA |

| Purpose | Reports distributions from HSAs/MSAs | Reports contributions to HSAs/MSAs |

| Issued By | Trustee or custodian | Trustee or custodian |

| Furnished By | January 31 | May 31 |

| Filed With IRS By | End of February (paper) / End of March (electronic) | End of May |

| Used By Taxpayer For | Reporting taxable or tax-free withdrawals | Verifying contributions |

| Filed With Tax Return? | Yes, if taxable | No |

Conclusion

Form 1099-SA may seem like just another tax form, but it plays a crucial role in maintaining the tax advantages of your health-related savings accounts. For custodians, accuracy and timely filing are essential to avoid penalties. For recipients, understanding whether distributions are taxable can prevent unpleasant surprises during tax season.