Facing a March 15th or April 15th tax deadline and your business return isn’t ready? Don’t panic—you’re not alone. Thousands of businesses file for extensions every year using IRS Form 7004.

Whether you’re an S corporation scrambling to gather K-1s, a partnership waiting on final numbers, or a C corporation dealing with complex deductions, Form 7004 can buy you up to 6 extra months. But filing it wrong could cost you thousands in penalties.

In this complete guide, you’ll learn exactly how to file Form 7004 for the 2025 tax year, avoid costly mistakes, and ensure you meet all IRS requirements.

What is Form 7004?

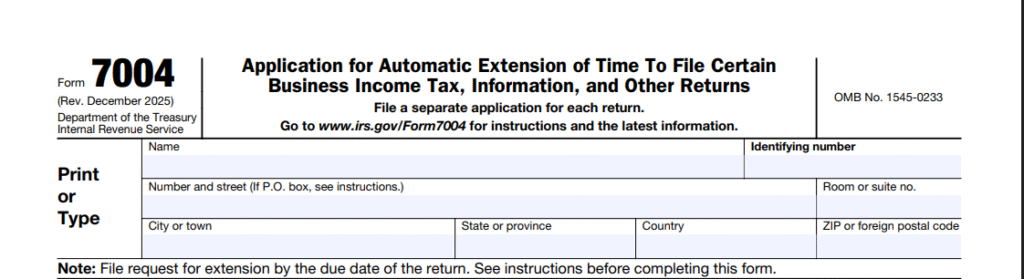

Form 7004 is an IRS extension form that allows businesses to request an automatic extension of time (generally up to 6 months) to file certain business income tax, information, and other returns.

It is important to note:

- Form 7004 extends the filing deadline, not the payment deadline.

- Any taxes due must still be paid by the original return due date to avoid interest and penalties.

- Once accepted, the extension is typically automatic—you do not need IRS approval unless there is a specific rejection.

Key Points You Must Understand:

✅ What Form 7004 DOES:

- Extends your filing deadline by 6 months (automatic approval)

- Prevents late filing penalties (5% per month, up to 25%)

- Gives you time to gather accurate information

- Costs nothing to file

❌ What Form 7004 DOES NOT DO:

- Does NOT extend your payment deadline (taxes still due on original date)

- Does NOT prevent interest charges on unpaid taxes

- Does NOT prevent late payment penalties if you don’t pay estimated taxes

- Does NOT provide a second extension (one extension only)

The Critical Mistake Most Businesses Make:

|

❌ WRONG: “I filed Form 7004, so I have 6 more months to pay my taxes.” |

|

✅ CORRECT: “I filed Form 7004, which gives me 6 more months to FILE, but I must PAY estimated taxes by the original deadline to avoid penalties.” |

The penalty for not paying: 0.5% per month (up to 25%) PLUS interest. On $50,000 in taxes, that’s $250/month in penalties alone.

Real-World Examples:

✅ ABC Corporation (S-Corp, calendar year) – CORRECT APPROACH

- Original deadline: March 15, 2026

- Files Form 7004: March 15, 2026

- Pays $25,000 estimated tax: March 15, 2026

- New filing deadline: September 15, 2026

- Result: $0 in penalties, $0 in interest

❌ XYZ Corporation (Makes This Mistake)

- Files Form 7004: March 15, 2026

- Pays $0 estimated tax: March 15, 2026

- Owes $25,000 in taxes

- Files return: September 15, 2026

- Penalty: $750 (6 months × 0.5% × $25,000)

- Interest: ~$750 (varies by IRS rate)

- Total cost of mistake: ~$1,500

Who Must File Form 7004?

Businesses that cannot meet their original filing deadlines for tax returns may file Form 7004. Entities that typically use this form include:

- C Corporations

- S Corporations

- Partnerships

- Multi-Member LLCs (treated as partnerships or corporations for tax purposes)

- Certain Trusts and Estates

- Nonprofit Organizations (for specific returns)

Essentially, any business entity required to file income tax or certain information returns (other than individuals) may need Form 7004.

What Type of Business Tax Forms Can Extend Using Form 7004?

Form 7004 covers a wide range of tax forms. Some of the most common include:

- Form 706-GS (D) – Generation-Skipping Transfer Tax Return for Distributions

- Form 706-GS (T) – Generation-Skipping Transfer Tax Return for Terminations

- Form 1041 – U.S. Income Tax Return for Estates and Trusts

- Form 1041-N – U.S. Income Tax Return for Electing Alaska Native Settlement Trusts

- Form 1041-QFT – U.S. Income Tax Return for Qualified Funeral Trusts

- Form 1042 – Annual Withholding Tax Return for U.S. Source Income of Foreign Persons

- Form 1065 – U.S. Return of Partnership Income

- Form 1066 – U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax Return

- Form 1120 – U.S. Corporation Income Tax Return

- Form 1120-C – U.S. Income Tax Return for Cooperative Associations

- Form 1120-F – U.S. Income Tax Return of a Foreign Corporation

- Form 1120-FSC – U.S. Income Tax Return of a Foreign Sales Corporation

- Form 1120-H – U.S. Income Tax Return for Homeowners Associations

- Form 1120-L – U.S. Life Insurance Company Income Tax Return

- Form 1120-ND – Return for Nuclear Decommissioning Funds and Certain Related Persons

- Form 1120-PC – U.S. Property and Casualty Insurance Company Income Tax Return

- Form 1120-POL – U.S. Income Tax Return for Certain Political Organizations

- Form 1120-REIT – U.S. Income Tax Return for Real Estate Investment Trusts

- Form 1120-RIC – U.S. Income Tax Return for Regulated Investment Companies

- Form 1120S – U.S. Income Tax Return for an S Corporation

- Form 1120-SF – U.S. Income Tax Return for Settlement Funds (Under Section 468B)

- Form 3520-A – Annual Information Return of Foreign Trust With a U.S. Owner

- Form 8612 – Return of Excise Tax on Undistributed Income of Real Estate Investment Trusts

- Form 8613 – Return of Excise Tax on Undistributed Income of Regulated Investment Companies

- Form 8725 – Excise Tax on Greenmail

- Form 8804 – Annual Return for Partnership Withholding Tax (Section 1446)

- Form 8831 – Excise Taxes on Excess Inclusions of REMIC Residual Interests

- Form 8876 – Excise Tax on Structured Settlement Factoring Transactions

- Form 8924 – Excise Tax on Certain Transfers of Qualifying Geothermal or Mineral Interests

- Form 8928 – Return of Certain Excise Taxes Under Chapter 43 of the Internal Revenue Code

📌 KEY TAKEAWAY: For 2025, the IRS has added Form 708 to the list of eligible returns. Form 708 calculates taxes under section 2801 for covered gifts or bequests from covered expatriates.

What are the Changes in Form 7004 for 2025 Tax Year?

The IRS has released the Final version of Form 7004 for the 2025 tax year with updates. Key changes include:

- Inclusion of Form 708 in the list of eligible returns.

- The form 708 is used to calculate and report taxes under section 2801 for covered gifts or bequests received from a covered expatriate.

Businesses should review the latest IRS instructions carefully to ensure they are filing correctly for 2025.

When is the Deadline to File Form 7004?

Deadlines for Form 7004 depend on the type of business entity and its tax year (calendar vs. fiscal year).

| Deadline | Applicable Forms |

| Business tax returns that are due by March 15, 2026 | Form 1120-S Form 1065 Form 1042 Form 1065-B Form 3520-A Form 8612 Form 8613 Form 8804 Form 1066 |

| Business tax returns that are due by April 15, 2026 | Form 1120 Form 1120-F Form 1120-FSC Form 1120-H Form 1120-L Form 1120-ND Form 1120-ND (Section 4951 taxes) Form 1120-PC Form 1120-POL Form 1120-REIT Form 1120-RIC Form 1120-SF Form 1041 (estate other than a bankruptcy estate) Form 1041 (bankruptcy estate only) Form 706-GS (D) Form 706-GS (T) Form 1041-N Form 1041-QFT Form 1041 (Trust) Form 1066 Form 8831 Form 8928 |

🗓️ Special Cases:

- Form 1120-C (Cooperatives): 15th day of 9th month after year-end

- Forms 8876, 8929, 8725: 90 days after tax year end

- Foreign corporations without US office: 15th day of 6th month after year-end

Important: Even with an extension, you must pay any taxes owed by the original deadline to avoid penalties.

Critical Deadline Table

| Entity Type | Original Deadline | Extension Due By | Final Deadline |

|---|---|---|---|

| S-Corp (calendar) | March 15 | March 15 | September 15 |

| Partnership (calendar) | March 15 | March 15 | September 15 |

| C-Corp (calendar) | April 15 | April 15 | October 15 |

⚠️ Remember: The extension must be filed ON OR BEFORE the original deadline!

How to Complete Form 7004 – Line by Line Instructions

Before you start, gather these:

- ☑️ Your EIN (Employer Identification Number)

- ☑️ Legal business name (exact match to IRS records)

- ☑️ Current year tax period dates

- ☑️ Estimated total tax liability for the year

- ☑️ Payments made to date (estimated tax payments, withholding)

Form 7004 at a Glance

Form 7004 has only 2 parts and 8 lines – it’s simpler than you think!

Part I: What return are you extending?

- Line 1: Enter the form code (e.g., “12” for Form 1120)

Part II: Your business information

- Lines 2-4: Special situations (office abroad, consolidated group, etc.)

- Line 5: Tax year dates

- Line 6: Total tax you expect to owe

- Line 7: Payments already made

- Line 8: Balance due (Line 6 minus Line 7)

That’s it! Now let’s go line by line…

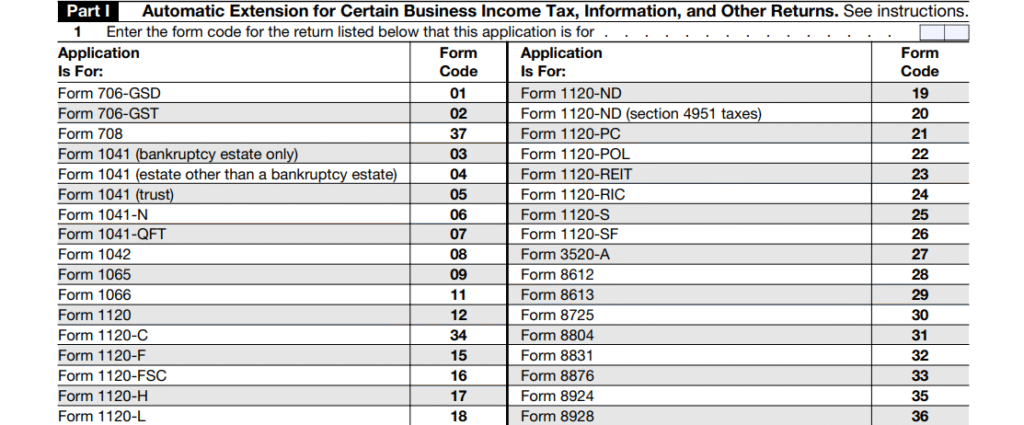

Part I: Automatic Extension for Certain Business Income Tax, Information, and Other Returns

Line 1: Form Code

Enter the appropriate form code in the boxes provided to indicate the return for which you are requesting an extension.

Common Form Codes:

| Code | Form | Description |

|---|---|---|

| 09 | 1065 | Partnership |

| 12 | 1120 | C Corporation |

| 25 | 1120-S | S Corporation |

| 04 | 1041 | Estate/Trust |

⚠️ Common Mistakes:

- ❌ Entering the wrong form code

- ❌ Using Form number instead of code (entering “1120” instead of “12”)

- ❌ Leaving this line blank

✅ Pro Tip: Double-check the form code table in the IRS instructions. The wrong code will cause rejection!

Important: If you are a trustee required to file Form 1041-A, you cannot use Form 7004. Instead, file Form 8868 to request an extension.

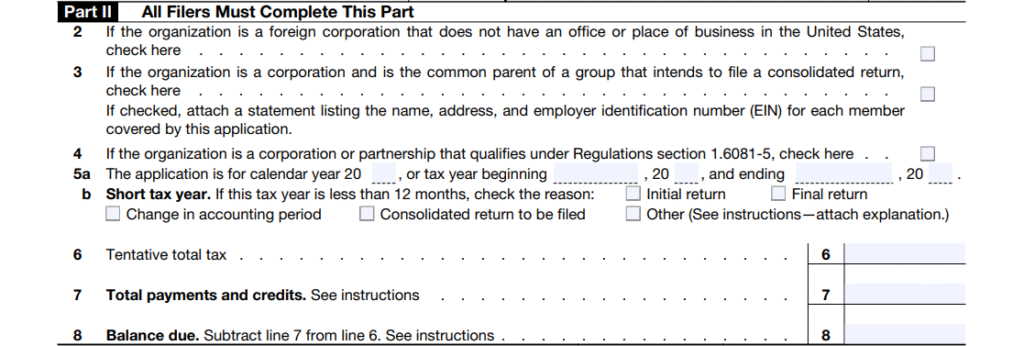

Part II: Information Required from All Filers

Line 2: Office or Place of Business Outside the U.S.

If your business maintains an office or place of business outside the United States and you are requesting an extension, check this box.

When to check this box:

- Your business has a physical office abroad

- You conduct business operations outside the U.S.

- Your principal place of business is outside the U.S.

Line 3: Consolidated Group Return

If you are the common parent or agent of a consolidated group requesting an extension for the group’s consolidated return, check this box.

Important: Attach a statement listing the name, address, and Employer Identification Number (EIN) of each member.

What is a consolidated group?

A parent corporation filing a single return that includes the income of all its subsidiaries.

Line 4: Automatic Extension Under Regulations Section 1.6081-5

Certain corporations and partnerships may qualify for an automatic extension under Regulations section 1.6081-5. If eligible, check this box.

Who qualifies?

- Partnerships keeping records outside the U.S. and Puerto Rico

- Domestic corporations conducting business and keeping records outside the U.S. and Puerto Rico

- Foreign corporations with a U.S. office or place of business

- U.S. citizens or residents with tax home outside the U.S.

Extension length: Until the 15th day of the sixth month following the close of the tax year

Line 5a: Tax Year Beginning and Ending Dates

If your business does not follow a calendar tax year, provide the beginning and ending dates of its tax year.

Examples:

- Calendar year: 01/01/2025 – 12/31/2025 (leave blank if calendar year)

- Fiscal year: 07/01/2025 – 06/30/2026 (must complete)

Line 5b: Short Tax Year

If your business has a short tax year, check the applicable box that explains the reason.

Reasons for short tax year:

- Initial return (first year of business)

- Final return (business ceasing operations)

- Change in accounting period

- Other (attach explanation)

📌 Note: If the short year is due to a change in accounting period, you must first obtain IRS approval (unless certain exceptions apply). For details, see Form 1128 and Publication 538.

Line 6: Tentative Total Tax

Enter the total tax liability expected for the year, including any nonrefundable credits.

How to estimate:

- Review prior year tax liability

- Adjust for known changes (income up/down, new deductions, etc.)

- Consult with accountant if significant changes

- Round to nearest dollar

Example Calculation:

- Prior year tax: $45,000

- Revenue up 20%: $45,000 × 1.20 = $54,000 estimated tax

- Enter on Line 6: $54,000

⚠️ Common Mistakes:

- ❌ Leaving Line 6 blank (required!)

- ❌ Using last year’s actual tax without adjusting

- ❌ Forgetting to include all taxes (not just income tax)

✅ Pro Tip: It’s better to OVERESTIMATE slightly. If you pay too much, you get a refund when you file. If you underestimate, you pay penalties and interest.

What to include in Line 6:

- ✅ Income tax

- ✅ Alternative minimum tax (if applicable)

- ✅ Any other taxes due with the return

- ❌ NOT refundable credits (subtract those)

Line 7: Total Payments and Refundable Credits

Enter the total payments and refundable credits for the year.

Include:

- Estimated tax payments made throughout the year

- Tax withholding (if applicable)

- Overpayments from prior year applied to current year

- Refundable credits

Example:

- Q1 estimated payment: $10,000

- Q2 estimated payment: $12,000

- Q3 estimated payment: $10,000

- Q4 estimated payment: $12,000

- Total on Line 7: $44,000

Line 8: Balance Due

Enter the balance due: Line 6 minus Line 7.

Calculation:

- Line 6 (Total tax): $54,000

- Line 7 (Payments): $44,000

- Line 8 (Balance): $10,000

🚨 CRITICAL: Form 7004 only extends the time to FILE, not the time to PAY. Any unpaid balance on Line 8 must be paid by the original due date to avoid penalties and interest.

If Line 8 is positive (you owe):

- Pay this amount by the original deadline

- Use EFTPS, IRS Direct Pay, or include payment with paper filing

- Failure to pay results in 0.5% monthly penalty + interest

If Line 8 is zero or negative:

- No payment needed with extension

- You’ll receive refund when you file actual return

Filing Options for Form 7004 Extension

You have two main options for filing Form 7004:

1. Electronic Filing (Recommended)

Benefits:

- ✅ Faster – confirmation within 24 hours

- ✅ More secure – encrypted transmission

- ✅ Automatic error checking

- ✅ Electronic confirmation you can save

- ✅ IRS requires many corporations to file electronically

- ✅ Can file and pay in one step

How to e-file:

- Choose an IRS-approved e-file provider

- Complete Form 7004 electronically

- Submit and pay (if balance due)

- Receive confirmation

2. Paper Filing

When to use:

- No access to e-file system

- Preference for paper records

- Small business with simple situation

Drawbacks:

- ❌ Slower – 2-4 weeks for processing

- ❌ Must mail to correct IRS address

- ❌ Requires certified mail for proof

- ❌ No automatic error checking

- ❌ Higher risk of processing delays

How to file by paper:

- Download Form 7004 from IRS.gov

- Complete by hand or fillable PDF

- Mail to correct address (see below)

- Use certified mail with return receipt

E-File vs Paper: Side-by-Side Comparison

| Feature | E-Filing | Paper Filing |

|---|---|---|

| Speed | 24 hours ✅ | 2-4 weeks |

| Confirmation | Instant ✅ | Certified mail receipt |

| Cost | Free ✅ | Postage + certified mail ($8-15) |

| Error checking | Built-in ✅ | Manual |

| Recommended? | YES ✅ | Only if no computer access |

💡 Our Recommendation: Always e-file unless you have no internet access. It’s faster, more accurate, and free.

Where to Mail Extension Form 7004?

If filing by mail, the address depends on your business location and whether you are including payment. Generally:

- With Payment – Mail to the IRS location specified for payment forms.

- Without Payment – Mail to the IRS service center for your state.

| Form – 1120-S, 1120, 1065, 1120-REIT, 1120-RIC, 8612, 8163 | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| Connecticut, Delaware, District of Columbia, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin | If the total assets at the end of the tax year are less than $10 million: Department of the Treasury, Internal Revenue Service, Kansas City, MO 64999-0019. If the total assets at the end of the tax year are $10 million or more: Department of the Treasury, Internal Revenue Service, Ogden, UT 84201-0045 |

| Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming | Department of the Treasury Internal Revenue Service Ogden, UT 84201-0045 |

| A foreign country or U.S. possession | Internal Revenue Service, P.O. Box 409101, Ogden, UT 84409. |

| Form 1041, 1120-H | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| Connecticut, Delaware, District of Columbia, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin | Department of the Treasury, Internal Revenue Service, Kansas City, MO 64999-0019. |

| Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming | Department of the Treasury, Internal Revenue Service, Ogden, UT 84201-0045. |

| A foreign country or U.S. possession | Internal Revenue Service, P.O. Box 409101, Ogden, UT 84409. |

| Form 706-GS(D), 706-GS(T) | |

| AND the settler is (or was at death) | Mailing Address to File Form 7004 |

| A resident U.S. citizen, resident alien, nonresident U.S. citizen, or alien | Department of the Treasury Internal Revenue Service Kansas City, MO 64999-0019 |

| Form 1041-QFT, 8725, 8831, 8876, 8924, 8928 | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| Any Location | Internal Revenue Service P.O. Box 409101 Ogden, UT 84409 |

| Form 1042, 1120-F, 1120-FSC, 3520-A, 8804 | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| Any Location | Internal Revenue Service P.O. Box 409101, Ogden, UT 84409 |

| Form 1066, 1120-C, 1120-PC | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| The United States | Department of the Treasury Internal Revenue Service Ogden, UT 84201-0045 |

| A foreign country or U.S. possession | Internal Revenue Service P.O. Box 409101 Ogden, UT 84409 |

| Form 1041-N, 1120-POL, 1120-L, 1120-ND, 1120-SF | |

| Principal Business, Office, or Agency Located in | Mailing Address to File Form 7004 |

| The United States | Department of the Treasury Internal Revenue Service Ogden, UT 84201-0045 |

| A foreign country or U.S. possession | Internal Revenue Service P.O. Box 409101 Ogden, UT 84409 |

⚠️ Important: The IRS provides a detailed chart in the Form 7004 instructions to determine the correct mailing address. Always verify before mailing!

What are the Penalties for Late Filing of Form 7004?

Failure to file Form 7004 on time—or failure to pay taxes due by the original deadline—may result in:

Penalty Structure

1. Late Filing Penalty (No Extension Filed)

- Rate: 5% of unpaid taxes per month

- Maximum: 25% of unpaid taxes

- Applies: When you don’t file Form 7004 AND miss your return deadline

Example:

- Tax owed: $50,000

- Months late: 3

- Penalty: $7,500 (5% × 3 × $50,000)

2. Late Payment Penalty

- Rate: 0.5% of unpaid taxes per month

- Maximum: 25% of unpaid taxes

- Applies: When you file Form 7004 but don’t pay estimated taxes by the original deadline

Example:

- Tax owed: $50,000

- Months late: 6 (extension period)

- Penalty: $1,500 (0.5% × 6 × $50,000)

3. Interest Charges

- Rate: Varies quarterly (currently ~8% annually)

- Compounds: Daily

- Applies to: All unpaid balances

Example:

- Tax owed: $50,000

- Period: 6 months

- Interest: ~$2,000 (varies by IRS rate)

Total Cost Comparison

| Scenario | Late Filing | Late Payment | Interest | Total Cost |

|---|---|---|---|---|

| Filed extension + paid taxes | $0 | $0 | $0 | $0 ✅ |

| Filed extension, didn’t pay (on $50K, 6 months) |

$0 | $1,500 | $2,000 | $3,500 |

| No extension, filed 6 months late (on $50K) |

$12,500 | $1,500 | $2,000 | $16,000 ❌ |

📌 KEY TAKEAWAY

Filing Form 7004 saves you money even if you can’t pay the full amount! The late filing penalty (5% per month) is 10x worse than the late payment penalty (0.5% per month).

Always file the extension, even if you can’t pay everything!

How to Minimize Penalties

- ✅ File Form 7004 by the original deadline

- ✅ Pay as much as you can by the original deadline (even partial payment helps)

- ✅ Set up a payment plan with the IRS if needed

- ✅ File your actual return within the extension period

Form 7004 vs Form 4868: Key Differences

One of the most common questions: “Is Form 7004 the same as Form 4868?”

One of the most common questions: “Is Form 7004 the same as Form 4868?”

Quick Answer: No. Form 7004 is for businesses; Form 4868 is for individuals.

Side-by-Side Comparison

| Feature | Form 7004 (Business) | Form 4868 (Individual) |

|---|---|---|

| Who Files | Corporations, Partnerships, LLCs | Individual taxpayers |

| Extends | Form 1120, 1120-S, 1065, others | Form 1040 |

| Extension Length | 6 months (typically) | 6 months |

| Original Deadline | March 15 or April 15 | April 15 |

| Extended Deadline | Sept 15 or Oct 15 | October 15 |

| Payment Required | Yes (estimated taxes) | Yes (estimated taxes) |

| E-file Available | Yes | Yes |

| Automatic Approval | Yes | Yes |

Common Confusion Scenarios

❓ “I own an S-Corp. Do I file Form 7004 or Form 4868?”

Answer: BOTH (if you need extensions for both)

- Form 7004 for your S-Corp business return (Form 1120-S)

- Form 4868 for your personal return (Form 1040)

These are completely separate extensions!

❓ “I’m a sole proprietor (Schedule C). Which form?”

Answer: Form 4868 only

- Sole proprietors file Schedule C with their Form 1040

- Business income is on your personal return

- Only need Form 4868

❓ “I have a single-member LLC. Which form?”

Answer: Depends on your tax classification

- Disregarded entity (default): Form 4868 (taxed on Schedule C)

- Elected S-Corp: Form 7004 (for 1120-S) + Form 4868 (for 1040)

- Elected C-Corp: Form 7004 only

Simple Rule to Remember:

- Business entity (Corp, Partnership) = Form 7004

- Personal tax return = Form 4868

- If you’re both a business owner and individual = possibly both

State Business Tax Extension Requirements

Federal Form 7004 extends your federal return, but most states require separate extensions. Here’s what you need to know:

⚠️ CRITICAL: Filing federal Form 7004 does NOT automatically extend your state return in most states!

States Requiring Separate Business Extensions

| State | Extension Form | Deadline | Auto-Extend with Federal? |

|---|---|---|---|

| California | FTB 3537 or CA Form 7004 | Same as federal | No ❌ |

| New York | CT-5 (corporations) IT-370 (partnerships) |

Same as federal | No ❌ |

| Illinois | IL-1120-EXT | Same as federal | No ❌ |

| Massachusetts | Form M-8736 | Same as federal | No ❌ |

| Pennsylvania | REV-276 | Same as federal | No ❌ |

States with No Income Tax (No Extension Needed)

Lucky you! These states have no business income tax:

- Alaska

- Florida (though gross receipts tax applies)

- Nevada

- South Dakota

- Texas (margin tax applies, but no income tax)

- Washington

- Wyoming

Action Steps for State Extensions

- ✅ File federal Form 7004

- ✅ Check your state’s requirements (most want a separate form)

- ✅ File state extension if needed (usually same deadline as federal)

- ✅ Pay any state taxes due

FAQs on IRS Form 7004

If you e-file, you’ll receive an IRS confirmation within 24 hours. For mailed forms, acceptance is assumed unless the IRS contacts you

No. Form 7004 provides only one automatic extension—no further extensions are available

1. Calendar Tax Period

A calendar tax period follows the traditional calendar year, starting on January 1 and ending on December 31. Most individuals and many small businesses use this period to report their income and file taxes.

Fiscal Tax Period

A fiscal tax period does not align with the calendar year. Instead, it is any 12-month period ending on the last day of any month other than December (for example, July 1 to June 30). Some businesses use a fiscal year because it better matches their natural business cycle, industry practices, or accounting needs.

Normally, the due date for S corporation returns (Form 1120-S) is the 15th day of the 3rd month following the end of the tax year.

For S corporations that operate on a calendar year basis, the deadline to file Form 7004 is March 17, 2026. Filing Form 7004 by this date grants S corporations an automatic six-month extension to submit their tax return, moving the filing deadline to September 15, 2026.

The IRS requires C corporations (filing Form 1120) to submit their returns by the 15th day of the 4th month after the end of the tax year.

For C corporations on a calendar tax year, the deadline to file Form 7004 is April 15, 2026. Filing Form 7004 by the original due date allows C corporations to receive an automatic six-month extension, pushing the final filing deadline to October 15, 2026 for calendar-year corporations.

Partnerships normally must file Form 1065 by the 15th day of the 3rd month after the end of their tax year.

For partnerships that follow the calendar year, the deadline to file Form 7004 is March 17, 2026. Filing Form 7004 by this date gives partnerships an automatic six-month extension, extending the return due date to September 15, 2026.

Yes, you must pay your estimated balance due when filing.

> EFTPS (Electronic Federal Tax Payment System)

> IRS Direct Pay

> Wire transfer

> Check or money order (with voucher)

This regulation grants an automatic extension until the 15th day of the sixth month following the close of the tax year for:

Partnerships keeping records outside the U.S. and Puerto Rico

Domestic corporations conducting business and keeping records outside the U.S. and Puerto Rico

Foreign corporations with a U.S. office or place of business

Domestic corporations whose primary income is derived from U.S. possessions

U.S. citizens or residents with a tax home and residence outside the U.S. and Puerto Rico

U.S. citizens in military or naval service stationed outside the U.S. and Puerto Rico

The perfection period is a limited window of time granted by the IRS to correct and resubmit a tax return or extension request (like Form 7004) that was rejected due to errors. If you fix the mistakes and refile within this timeframe—generally 5 calendar days for electronic filings—the IRS will consider the submission as if it was filed on the original deadline, helping you avoid late-filing penalties.

When filing Form 7004 electronically, the IRS system may reject your submission for various reasons. Common rejection types include:

1. EIN and Name Mismatch (Error Code R0000-922-01)

The Employer Identification Number (EIN) and legal business name do not match IRS records.

Fix: Verify the EIN and business name against your IRS EIN confirmation letter.

2. Invalid Form Code (Error Code R0000-922-02)

The code entered on Line 1 of Form 7004 does not correspond to the return type.

Fix: Double-check the IRS instructions and enter the correct form code (e.g., “12” for Form 1120).

3. Duplicate Filing (Error Code R0000-905-01)

An extension request for the same business, form, and tax year has already been filed.

Fix: Check if another filing was submitted before; no second request is allowed.

4. Late Submission (Error Code R0000-194-01)

The request was filed after the original due date of the return.

Fix: Extensions must be filed on or before the due date of the return; once late, Form 7004 cannot be used.

5. Invalid Tax Year (Error Code R0000-147-01)

The tax year entered does not match the business’s filing period or IRS records.

Fix: Ensure the correct beginning and ending dates of the tax year are entered in Part II, Line 5a.

No, you cannot file Form 7004 without a valid EIN. The IRS processing systems for business extensions are automated and require a matching EIN to identify the tax account. If you have applied for an EIN but haven’t received it, you should not leave the space blank or use a Social Security Number. Instead, wait until the EIN is assigned. If the tax deadline is approaching and you still don’t have an EIN, you may need to file a paper return (not an extension) with “Applied For” written in the EIN section, though it is highly recommended to call the IRS identity verification line first to expedite your number.

If your electronic Form 7004 is rejected, the IRS typically provides a “perfection period” of 5 calendar days to correct the error and re-file. To qualify for this grace period, the initial filing must have been made on or before the due date. Common reasons for rejection include a name control mismatch (the business name doesn’t match IRS records) or an incorrect Form Code in Part I. Fix the specific error code provided in your rejection notice and re-transmit immediately to avoid late-filing penalties.

Yes. If your business terminated operations during the year, your final tax return is due by the 15th day of the 3rd month after the date of dissolution. For example, if you dissolved on June 30th, your return is due September 15th. If you cannot meet that “short year” deadline, you must file Form 7004 to get an extension. When filing, ensure you check the “Short Tax Year” box (Line 5b) and provide the reason (e.g., “Final Return”) to ensure the IRS doesn’t flag your account for a missing future return.

Not necessarily. This is a common trap for business owners. While many states (like Texas or Pennsylvania) recognize the Federal extension automatically, others (like New York or California) may require their own specific state form or a copy of the Federal 7004 to be attached to the state return later. Always check your specific state’s Department of Revenue requirements. Filing Form 7004 protects you from IRS penalties, but it does not protect you from state-level late filing fees.