For small nonprofits navigating the complex world of IRS compliance, Form 990-EZ serves as a critical annual reporting tool. Whether you are a newly formed charitable organization, a social club, or a religious association, understanding Form 990-EZ is essential for maintaining your tax-exempt status and staying in good standing with the IRS.

This comprehensive guide covers everything — from what the form is and who must file, to deadlines, e-filing requirements, penalties, and step-by-step instructions. Read on to ensure your organization files correctly, on time, and without costly mistakes.

What Is Form 990-EZ?

Form 990-EZ, officially titled “Short Form Return of Organization Exempt From Income Tax,” is an annual information return that small tax-exempt organizations must file with the Internal Revenue Service (IRS). It is a shorter, simplified version of the full Form 990, designed specifically for organizations with gross receipts under $200,000 and total assets under $500,000 at the end of the tax year.

Despite its name suggesting simplicity, Form 990-EZ is a comprehensive document. It collects information about your organization’s revenue, expenses, assets, liabilities, program accomplishments, governance structure, key officers, and compliance with various IRS regulations.

Purpose of Form 990-EZ

The IRS uses Form 990-EZ to:

- Verify that your organization continues to qualify for tax-exempt status

- Ensure the organization’s activities align with its stated tax-exempt purpose

- Provide transparency to the public — Form 990-EZ is publicly available and can be viewed by donors, watchdog groups, and the general public

- Collect data on the nonprofit sector for regulatory and statistical purposes

Unlike for-profit businesses that file income tax returns, tax-exempt organizations generally do not pay income tax. However, they are still required to file an annual information return to maintain transparency and accountability.

Who Must File Form 990-EZ?

Not every nonprofit files Form 990-EZ. The IRS has specific thresholds that determine which version of Form 990 an organization must file.

Eligibility Criteria for Form 990-EZ

Your organization qualifies to file Form 990-EZ if ALL of the following conditions are met:

- Gross receipts are at least $50,000 but less than $200,000 for the tax year

- Total assets at the end of the tax year are less than $500,000

- The organization is tax-exempt under IRC Section 501(c), 527, or 4947(a)(1)

Types of Organizations Required to File Form 990-EZ

- Charitable organizations — 501(c)(3) public charities

- Social welfare organizations — 501(c)(4)

- Labor and agricultural organizations — 501(c)(5)

- Business leagues and chambers of commerce — 501(c)(6)

- Social and recreational clubs — 501(c)(7)

- Fraternal beneficiary societies — 501(c)(8)

- Veterans’ organizations — 501(c)(19)

- Political organizations under Section 527 that meet the gross receipts threshold

- Nonexempt charitable trusts under Section 4947(a)(1)

Who Is Exempt From Filing Form 990-EZ?

- Churches, conventions of churches, and associations of churches

- Integrated auxiliaries of churches

- Organizations with gross receipts normally $50,000 or less — they file Form 990-N instead

- Private foundations — they file Form 990-PF instead

- U.S. government instrumentalities

- State institutions whose income is excluded under IRC Section 115

Which Form Should You File? Quick Reference Guide

Use the table below to quickly determine the correct form for your organization based on gross receipts and total assets:

| Gross Receipts | Total Assets (Year-End) | Correct Form to File |

|---|---|---|

| $50,000 or less | Any amount | Form 990-N (e-Postcard) |

| $50,001 to $199,999 | Less than $500,000 | Form 990-EZ |

| $200,000 or more | Any amount | Form 990 (Full) |

| Any amount | $500,000 or more | Form 990 (Full) |

| Any amount (Private Foundation) | Any amount | Form 990-PF |

Real-World Examples: Choosing the Right Form

Example 1: Small Animal Rescue Nonprofit

Paws & Hope Animal Rescue is a 501(c)(3) organization. In 2024, it raised $85,000 in donations and had total assets of $42,000 at year-end. Gross receipts = $85,000 (between $50,001 and $199,999) + Total assets = $42,000 (under $500,000) → FILES FORM 990-EZ

Example 2: Tiny Community Garden Club

The Riverside Garden Club is a 501(c)(7) social club. In 2024, it collected $8,500 in membership dues and held no significant assets. Gross receipts = $8,500 (at or below $50,000) → FILES FORM 990-N (e-Postcard) — not Form 990-EZ

Example 3: Growing Regional Food Bank

Second Harvest Food Network is a 501(c)(3). In 2024, it received $350,000 in grants and donations, and held $620,000 in food inventory and equipment. Gross receipts = $350,000 (exceeds $200,000) AND total assets = $620,000 (exceeds $500,000) → FILES FORM 990 (Full Form)

Example 4: Local Veterans Organization

American Veterans Post 44 is a 501(c)(19). In 2024, it raised $175,000 through fundraising events and held $280,000 in assets. Gross receipts = $175,000 (between $50,001 and $199,999) + Total assets = $280,000 (under $500,000) → FILES FORM 990-EZ

Example 5: Private Family Foundation

The Henderson Family Foundation is a private foundation under 501(c)(3). It has assets of $1.2 million and distributed $90,000 in grants in 2024. Regardless of gross receipts or asset size — Private foundations always FILE FORM 990-PF

Important Note on Thresholds

If your organization normally files Form 990-N but had an unusually high revenue year that pushed gross receipts above $50,000, you may need to file Form 990-EZ for that year. Always base your filing decision on the actual gross receipts and total assets for the specific tax year being reported.

When Is the Deadline to File Form 990-EZ?

Filing Form 990-EZ on time is critical. Missing the deadline can result in automatic penalties and, in some cases, automatic revocation of your tax-exempt status.

Standard Filing Deadline

Form 990-EZ is due by the 15th day of the 5th month after the end of your organization’s accounting period (fiscal year).

| Fiscal Year End | Standard Due Date | Extended Due Date (with Form 8868) |

|---|---|---|

| January 31 | June 15 | December 15 |

| February 28/29 | July 15 | January 15 |

| March 31 | August 15 | February 15 |

| April 30 | September 15 | March 15 |

| May 31 | October 15 | April 15 |

| June 30 | November 15 | May 15 |

| July 31 | December 15 | June 15 |

| August 31 | January 15 | July 15 |

| September 30 | February 15 | August 15 |

| October 31 | March 15 | September 15 |

| November 30 | April 15 | October 15 |

| December 31 | May 15 | November 15 |

Most Common Fiscal Year

The majority of nonprofits operate on a calendar year (January 1 to December 31). For these organizations, Form 990-EZ is due May 15 each year, with an extended deadline of November 15 if Form 8868 is e-filed by May 15.

Automatic Extension: Form 8868

If your organization needs more time, you can request an automatic 6-month extension by e-filing Form 8868 (Application for Automatic Extension of Time To File an Exempt Organization Return) by the original due date.

- The extension is automatic — no IRS approval required

- No reason or explanation is needed

- Extends the filing deadline only, not any tax payment due

- For calendar-year filers, the extended deadline becomes November 15

- Form 8868 must also be e-filed — paper submission is not accepted

Important Warning

Even with an approved extension, if your organization fails to file for three consecutive years, the IRS will automatically revoke your tax-exempt status. Reinstatement requires a formal application process and back-filing.

What Information Is Required to Complete Form 990-EZ?

Form 990-EZ consists of several parts and schedules. Here is a detailed breakdown of every piece of information you will need to gather before you begin.

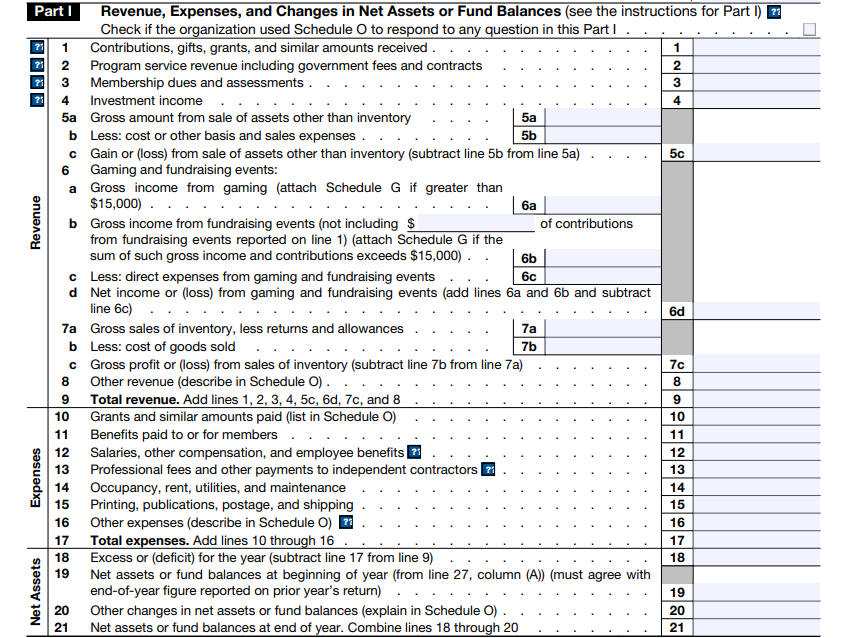

Part I — Revenue, Expenses, and Changes in Net Assets

This section requires a full accounting of your organization’s financial activity for the tax year:

- Contributions, gifts, grants, and similar amounts received

- Program service revenue — fees charged for services related to your exempt purpose

- Membership dues and assessments

- Investment income — interest, dividends, rents, royalties

- Sale of assets — cost basis and sale proceeds

- Special event gross income and direct expenses

- Gross profit or loss from sales of inventory

- Other revenue and total revenue

Expenses:

- Grants and similar amounts paid, benefits paid to members

- Salaries, other compensation, and employee benefits

- Professional fees and payments to independent contractors

- Occupancy, rent, utilities, and maintenance

- Printing, publications, postage, and shipping

- Total expenses, net surplus or deficit, and beginning and ending net assets

Part II — Balance Sheet

- Cash, savings, and investments

- Land, buildings, and equipment (net of depreciation)

- Other assets and total assets

- Accounts payable, loans, and other liabilities

- Net assets or fund balances at beginning and end of year

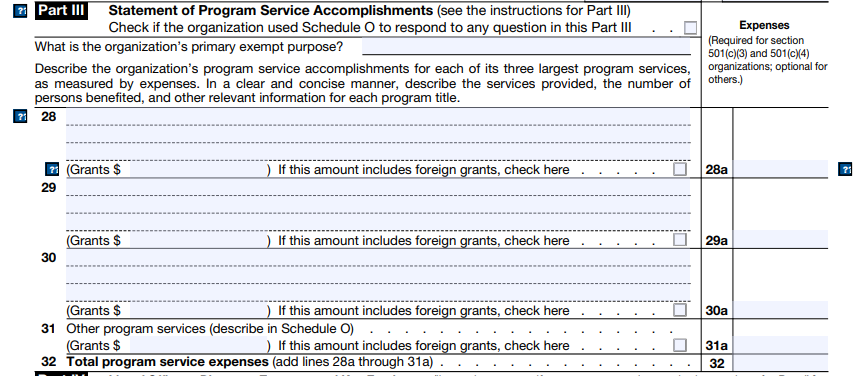

Part III — Statement of Program Service Accomplishments

- Description of each of the three largest program services

- Number of people served or measurable outputs achieved

- Grants awarded under each program (if applicable)

- Revenue and expenses attributable to each program

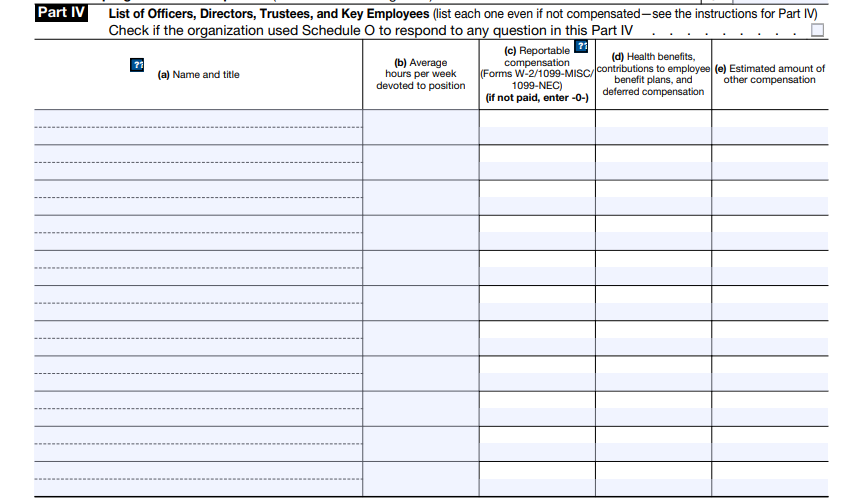

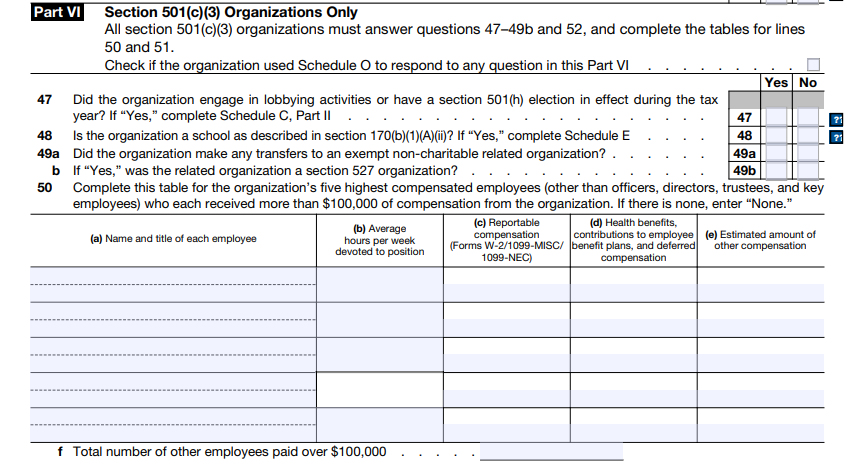

Part IV — Officers, Directors, Trustees, and Key Employees

- Name and title of each person who served during the tax year

- Average hours per week devoted to the position

- Reportable compensation from the organization and related organizations

- Estimated amount of other compensation

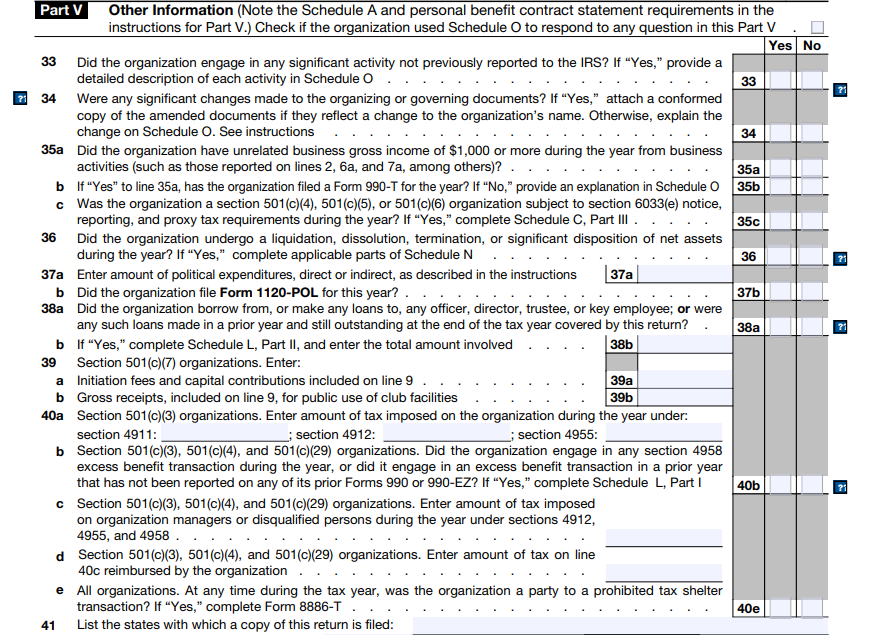

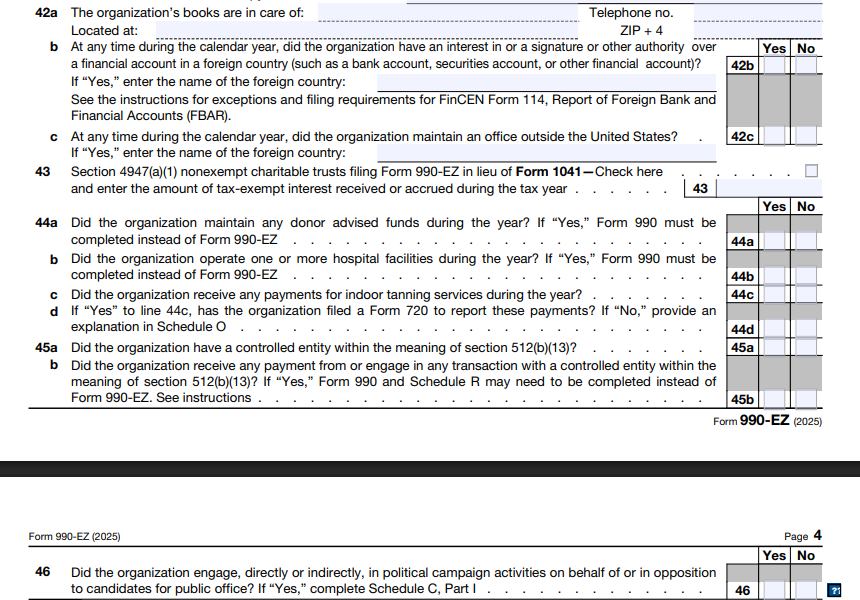

Part V — Other Compliance Information

- Whether the organization engaged in activities not previously reported to the IRS

- Whether governing documents were changed

- Whether the organization had unrelated business income

- Whether the organization was party to a prohibited tax shelter transaction

- Whether the organization received in-kind property or services

Part VI — Section 501(c)(3) Organizations Only

- Family or business relationships between officers, directors, trustees, or key employees

- Whether a written conflict of interest policy was followed

- Whether the governing body reviewed the Form 990-EZ before filing

- Whether meetings were contemporaneously documented

- Whether the organization became aware of a significant diversion of assets

General Organization Information Required

- Legal name and DBA name, if applicable

- Mailing address and EIN (Employer Identification Number)

- Organization’s fiscal year and type of return — initial, final, or amended

- Tax-exempt code section (e.g., 501(c)(3)) and website address

Unrelated Business Income (UBI) and Form 990-T Filing Requirements

One of the most commonly misunderstood aspects of nonprofit tax compliance is unrelated business income (UBI). Even tax-exempt organizations can be subject to federal income tax if they earn income from activities that are not substantially related to their exempt purpose. Understanding UBI is essential because it directly affects your Form 990-EZ filing and may trigger a separate tax return obligation.

What Is Unrelated Business Income?

Unrelated Business Income is income from a trade or business that meets all three of the following IRS criteria:

- It is a trade or business — the activity involves the sale of goods or services for income

- It is regularly carried on — the activity occurs with the same frequency and continuity as a comparable commercial operation

- It is not substantially related to the organization’s exempt purpose — beyond simply providing funds for the mission

The key question is not what the money is used for, but where it comes from. Even if every dollar of UBI is reinvested into your mission, the income itself may still be taxable.

UBI Exclusions and Exceptions

Not all commercial-looking activity creates UBI. The IRS provides important statutory exclusions:

- Dividends, interest, annuities, royalties, and most rents are excluded from UBI as passive income

- Income from activities conducted entirely by unpaid volunteers is excluded

- Income from activities conducted for the convenience of members, students, patients, or employees is excluded

- Income from the sale of donated merchandise is excluded

- Specific games of chance such as bingo are excluded by statute

The $1000 Threshold: When Must You File Form 990-T?

If your organization has gross UBI exceeding one thousand dollars in a tax year, you are required to file Form 990-T (Exempt Organization Business Income Tax Return) in addition to Form 990-EZ. Form 990-T is a separate return that calculates the Unrelated Business Income Tax (UBIT) your organization owes.

| Gross UBI Amount | Action Required |

|---|---|

| Under $1000 | No Form 990-T required; still disclose UBI activity on Form 990-EZ Part V |

| $1000 or more | Must file Form 990-T AND pay Unrelated Business Income Tax (UBIT) at 21% |

Important: Gross vs. Net UBI

The threshold applies to gross UBI before expenses, not net UBI. Even if your organization has zero net profit after deducting business expenses, you must still file Form 990-T if gross UBI exceeds the threshold.

How Is UBI Taxed?

Unrelated Business Income is taxed at the flat corporate income tax rate of 21 percent on net UBI — gross UBI minus allowable deductions directly connected to the unrelated business activity. Common allowable deductions include:

- Salaries and wages directly attributable to the unrelated business

- Depreciation on assets used in the unrelated business activity

- Advertising and marketing costs specific to the unrelated business

- A specific deduction of one thousand dollars is automatically allowed per unrelated trade or business

If your organization operates multiple separate unrelated business activities, each must be tracked and reported separately on Form 990-T. Losses from one unrelated business generally cannot offset income from another.

Form 990-T: Deadline and E-Filing Requirement

Form 990-T is due on the same date as Form 990-EZ — the 15th day of the 5th month after the close of the tax year. For calendar-year organizations, this is May 15. An automatic 6-month extension is available by e-filing Form 8868, but any tax owed must be paid by the original due date even if an extension is granted.

Form 990-T must also be e-filed. The IRS does not accept paper Form 990-T returns.

UBI Compliance Warning

Failing to report UBI or failing to file Form 990-T when required can result in penalties, back taxes, and interest charges. Repeated or willful failure to report UBI could be grounds for revocation of tax-exempt status. Consult a nonprofit tax professional if you are uncertain whether an income source constitutes UBI.

How UBI Is Disclosed on Form 990-EZ?

Even if UBI is below the filing threshold and Form 990-T is not required, you must still acknowledge unrelated business activities on Form 990-EZ:

- Part V, Line 33 asks whether the organization had UBI of one thousand dollars or more during the year

- If yes, you must confirm that Form 990-T was filed

- Revenue from unrelated business activities should be reported in Part I under Other Revenue

- Maintain detailed records year-round to accurately distinguish related from unrelated business income

State Unrelated Business Income Tax

Many states impose their own state-level unrelated business income tax in addition to the federal UBIT. Requirements vary significantly — some states conform to the federal UBI definition while others have distinct rules and thresholds. Always consult your state department of revenue or a local tax advisor to determine whether state UBIT filings apply.

What Are the Additional Filing Requirements with Form 990-EZ?

Depending on your organization’s activities and type, you may need to attach one or more schedules to Form 990-EZ.

Required Schedules

| Schedule | Who Must File |

|---|---|

| Schedule A | 501(c)(3) organizations — public charity status and public support test |

| Schedule B | Organizations receiving contributions of $5,000 or more from any one contributor |

| Schedule C | Organizations engaging in political campaign activities or lobbying |

| Schedule E | Private schools — nondiscrimination policy disclosure |

| Schedule G | Organizations reporting more than $15,000 from fundraising events or gaming |

| Schedule L | Organizations with loans or transactions involving interested persons |

| Schedule N | Organizations that liquidated, terminated, or significantly contracted |

| Schedule O | Supplemental information for any line of Form 990-EZ |

State Filing Requirements

In addition to the federal Form 990-EZ, many states require nonprofits to file a separate state annual report or registration renewal. Requirements vary by state. Always check with your state attorney general’s office or secretary of state to confirm your specific obligations.

Public Disclosure Requirements

- Form 990-EZ must be available for public inspection during regular business hours

- Copies must be provided to anyone who requests them — a reasonable copying fee may be charged

- The IRS makes these returns publicly available through its Tax Exempt Organization Search database

- Third-party platforms such as ProPublica and GuideStar (Candid) also publish 990s

How to File Form 990-EZ?

Form 990-EZ must be e-filed. There is no paper filing option. Here is a step-by-step guide to completing and submitting your return electronically.

Step 1: Gather Your Financial Records

- Income statements and bank statements for the tax year

- Expense records and receipts

- Payroll records for officer compensation

- Investment account statements

- Prior year Form 990-EZ for reference and comparison

- List of officers, directors, and trustees with compensation details

- Program service accomplishment descriptions

Step 2: E-File Your Return — This Is Mandatory

E-filing is mandatory for Form 990-EZ. Paper filing is not permitted under any circumstances. Under the Taxpayer First Act of 2019, all tax-exempt organizations are required to file their Form 990-series returns electronically. This requirement applies to every organization regardless of size, gross receipts, or number of returns filed. There are no exceptions.

Paper Filing Is Not Allowed

The IRS will not accept Form 990-EZ submitted on paper. Do not attempt to mail a paper return — it will not be processed, and your organization will be treated as having failed to file. This can trigger late filing penalties and, after three consecutive years, automatic revocation of your tax-exempt status. You must e-file through an IRS-authorized provider.

How to E-File Form 990-EZ

- Use an IRS-authorized e-file provider, also known as an Electronic Return Originator (ERO)

- A number of IRS-authorized third-party e-file providers offer guided, step-by-step software designed specifically for tax-exempt organization returns — the full list of authorized providers is available at IRS.gov

- These platforms offer guided, step-by-step software designed specifically for tax-exempt organization returns

- Upon submission, you receive an immediate electronic acknowledgment confirming IRS receipt

- Built-in validation checks catch common errors before your return is transmitted

- Fees typically range from $40 to $200 depending on return complexity and schedules required

Benefits of E-Filing

- Instant IRS confirmation of receipt — eliminates uncertainty about whether your return arrived

- Faster processing compared to paper returns

- Automatic error detection reduces the risk of IRS rejection or follow-up correspondence

- Secure, encrypted transmission of your organization’s financial data

- Digital copies are easy to store and retrieve for future audits or grant applications

Step 3: Complete the Form Sections in Order

- Enter your organization’s basic information at the top of the form

- Complete Part I — Revenue and Expenses using your financial records

- Complete Part II — Balance Sheet as of the first and last day of the tax year

- Complete Part III — Program Service Accomplishments

- Complete Part IV — Officers, Directors, Trustees, and Key Employees

- Answer all questions in Part V — Other Information

- Complete Part VI if your organization is a 501(c)(3)

- Attach all required schedules

- Electronically sign and date the return as an authorized officer

Step 4: Review Before Submitting

- Verify all calculations

- Confirm EIN, organization name, and address are correct

- Ensure all required schedules are attached

- Check that revenues and expenses reconcile to the balance sheet

- Confirm all yes/no questions in Parts V and VI are answered

- Confirm the return is electronically signed by an authorized officer

Step 5: Submit and Save Your Confirmation

- Submit your e-filed return through the authorized provider by the due date

- Save the electronic acknowledgment from the IRS as proof of timely filing

- Retain a complete copy of the filed return and all supporting documents for at least 3 years — 7 years is recommended

Pro Tip: Consider Professional Help

If your organization is new to filing or has complex financials, consider working with a CPA or enrolled agent with nonprofit tax experience. Many nonprofit-focused accountants are familiar with IRS-authorized e-filing platforms and can handle the submission on your behalf.

What Are the Penalties for Missing Form 990-EZ?

The IRS imposes significant penalties for late filing, failure to file, and failure to include required information. Understanding these penalties underscores the importance of e-filing on time and accurately.

Late Filing Penalty

| Organization Type | Daily Penalty | Maximum Penalty |

|---|---|---|

|

Gross receipts under $1,208,500

|

$20 per day

|

$12,000 or 5% of gross receipts, whichever is less

|

|

Gross receipts $1,208,500 or more

|

$120 per day

|

$60,000

|

Failure to Include Required Information

If the return is filed but incomplete — missing schedules, missing electronic signature, or containing incorrect information — the IRS can impose the same daily $20 penalty until a complete, corrected return is received.

Penalty on Responsible Persons

If an officer or other responsible person willfully failed to file or provided false information, that individual can be personally liable for a penalty of $10 per day, up to $5,000 per return.

Automatic Revocation of Tax-Exempt Status

Under the Pension Protection Act of 2006, any tax-exempt organization that fails to file a required annual return for three consecutive years will automatically lose its tax-exempt status.

- Revocation takes effect on the due date of the third consecutive missed return

- The IRS publishes a list of automatically revoked organizations on its website

- Donors who contributed to a revoked organization may lose their charitable deduction

- The organization becomes subject to income tax on all income during the revocation period

Reinstatement After Revocation

- File a new exemption application — Form 1023 or 1023-EZ for 501(c)(3), or the appropriate form for other types

- Pay the applicable IRS user fee

- Submit a statement explaining why the organization failed to file and what corrective steps have been taken

Small organizations with gross receipts of $50,000 or less may qualify for a simplified reinstatement procedure if they apply within 15 months of the date of the revocation notice.

Critical Warning: Revocation Has Real Consequences

Automatic revocation affects donors’ tax deductions, jeopardizes foundation grants, triggers state-level compliance issues, and damages organizational credibility. E-file on time, every year — no exceptions.

Penalty Abatement

If your organization has reasonable cause for failing to file on time — such as a natural disaster, serious illness of the responsible party, or destruction of records — you may request penalty abatement by attaching a written explanation to the late-filed return or by contacting the IRS directly. First-time penalty abatement may also be available for organizations with a clean prior compliance history.

Additional Tips and Best Practices for Filing Form 990-EZ

Maintain Good Recordkeeping Throughout the Year

- Reconcile bank accounts monthly

- Use nonprofit accounting software such as QuickBooks Nonprofit, Wave, or Aplos

- Document all grants received and awarded

- Maintain a chart of accounts that clearly separates program, management, and fundraising expenses

Have Your Governing Board Review the Return Before Filing

IRS Form 990-EZ asks whether the governing body reviewed the return before it was filed. Best practice is to share a draft with your board of directors before e-filing. This promotes accountability, reduces errors, and is increasingly required for grant eligibility.

Choose Your E-File Provider Early

Research IRS-authorized e-file providers well before the deadline. Compare pricing, confirm the platform supports all the schedules your organization requires, and create your account in advance to avoid last-minute technical issues.

Update Your Organization’s Information with the IRS

- Address change: Check the appropriate box on Form 990-EZ or file Form 8822-B

- Name change: Notify the IRS in writing or directly on the return

- Accounting period change: File Form 1128 (Application to Adopt, Change, or Retain a Tax Year)

Verify Your Status in the IRS Tax Exempt Organization Search

Periodically confirm your organization appears in the IRS Tax Exempt Organization Search (TEOS) database with an active, valid status. This is the same database donors use to verify that contributions are tax-deductible.

Frequently Asked Questions About Form 990-EZ

Can a new nonprofit skip filing Form 990-EZ in its first year?

No. Most tax-exempt organizations must file for every tax year in which they hold exempt status, including their first year. If gross receipts are normally $50,000 or less, the organization may file Form 990-N instead.

Can I file Form 990-EZ on paper?

No. Paper filing is not permitted for Form 990-EZ under any circumstances. The Taxpayer First Act of 2019 requires all tax-exempt organizations to file electronically through an IRS-authorized e-file provider. A paper return will not be processed by the IRS and will be treated as a failure to file, potentially triggering penalties.

What if my organization’s gross receipts go over $200,000?

If gross receipts for the tax year reach $200,000 or more, or if total assets reach $500,000 or more at year-end, the organization must file the full Form 990 — not Form 990-EZ.

Is Form 990-EZ the same as an income tax return?

No. Form 990-EZ is an information return, not an income tax return. Tax-exempt organizations generally do not pay federal income tax on income related to their exempt purpose. However, if the organization has unrelated business income (UBI) exceeding $1,000, it must also file Form 990-T.

Can I amend a previously filed Form 990-EZ?

Yes. File an amended return by checking the ‘Amended Return’ box at the top of the form and attaching a statement explaining what changed and why. Amended returns must also be e-filed.

Does Form 990-EZ need to be signed?

Yes. Form 990-EZ must be electronically signed by an authorized officer — such as the president, vice president, treasurer, or chief financial officer. An unsigned return is not considered filed.

How much does it cost to e-file Form 990-EZ?

Most IRS-authorized e-file platforms charge between $40 and $200 for Form 990-EZ, depending on the complexity of the return and the number of schedules required. This is a legitimate organizational expense.

What is the difference between Form 990-EZ and Form 990-N?

Form 990-N (e-Postcard) is an extremely simple annual notice for organizations with gross receipts of $50,000 or less. It only requires basic information such as the organization’s name, EIN, address, and confirmation that receipts are below the threshold. Form 990-EZ is a full short-form return requiring detailed financial statements, program descriptions, and officer disclosures, filed by organizations with gross receipts between $50,001 and $199,999.

Conclusion

Form 990-EZ is more than a compliance requirement — it is a public record that reflects your organization’s integrity, governance, and financial health. Filing accurately and on time demonstrates accountability to donors, grantors, and the communities you serve.

Remember: e-filing is mandatory for Form 990-EZ. Paper returns are not accepted under any circumstances. Choose an IRS-authorized e-file provider, maintain organized records throughout the year, and never let three consecutive years pass without filing — the consequences of automatic revocation are simply too severe.

With the right preparation and tools, Form 990-EZ is entirely manageable. Use this guide as your annual reference and approach each filing season with confidence.

Need Help Filing Form 990-EZ?

Consider working with a CPA or enrolled agent experienced in nonprofit tax compliance. You can also use an IRS-authorized third-party e-file provider that offers guided software specifically designed for exempt organization returns. A complete and current list of authorized providers is available at IRS.gov.