In accounting, one fundamental principle governs all financial records and transactions — the accounting equation. It’s the bedrock of the double-entry bookkeeping system and provides a snapshot of a company’s financial health at any given point. Every financial transaction a business makes must keep this equation in balance. Without understanding this equation, it’s nearly impossible to grasp the structure of financial statements or the logic behind accounting processes.

This guide explores the accounting equation in depth, explaining each component, how it works, how it’s used in real-life financial reporting, and why it’s critical for ensuring the integrity of business records

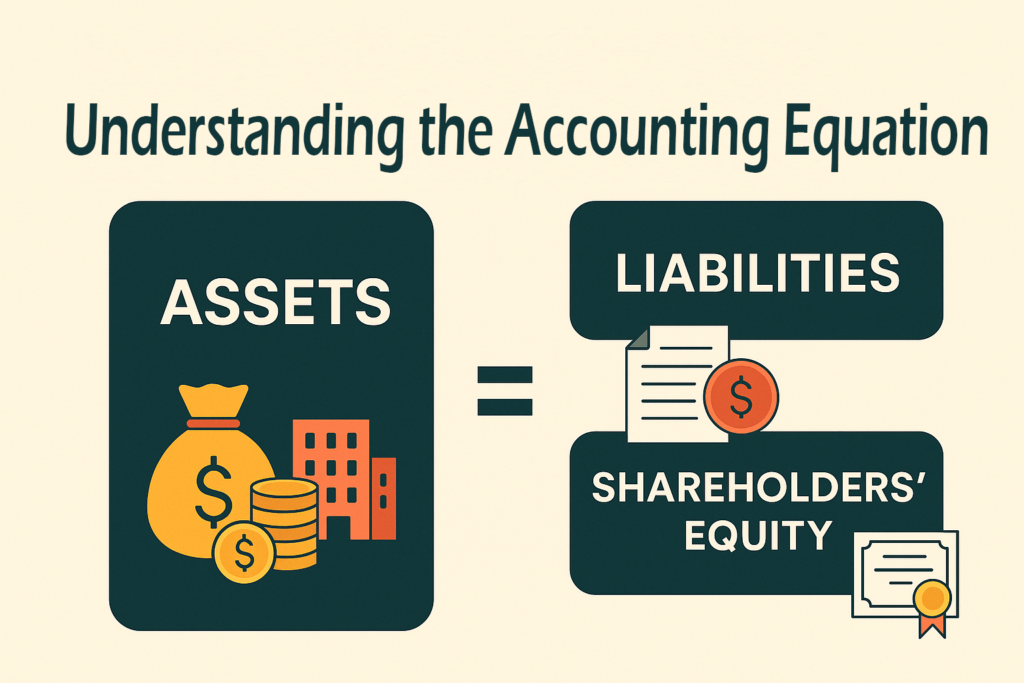

What Is the Accounting Equation?

The accounting equation is a basic yet powerful expression that shows the relationship between a company’s assets, liabilities, and shareholders’ equity. It forms the foundation of the double-entry system, which requires that every transaction affect at least two accounts in a way that keeps the equation in balance.

The Accounting Equation:

Assets = Liabilities + Shareholders’ Equity

This equation reflects the idea that all the resources owned by a business (assets) are financed either through debt (liabilities) or through the owner’s investment (equity). In simple terms, what a business owns must always equal what it owes plus what the owners have invested.

Even though this concept appears simple, it underpins all accounting systems, from small businesses to multinational corporations.

How the Accounting Equation Works

Let’s break down each of the three elements of the accounting equation and explore what they represent in the financial structure of a business.

Assets

Assets are everything a company owns that has value and can be used to generate revenue. This includes both tangible and intangible items.

Examples of assets include:

- Cash and cash equivalents

- Inventory

- Equipment and machinery

- Vehicles

- Real estate or buildings

- Accounts receivable

- Intellectual property (e.g., patents, trademarks)

Assets are often categorized as:

- Current Assets (expected to be used or converted into cash within a year)

- Non-Current Assets (long-term resources like property, plant, and equipment)

Assets increase when a company earns revenue, makes investments, or receives loans. They decrease when the company pays off debt, incurs losses, or distributes dividends.

Liabilities

Liabilities are obligations or debts a business owes to other entities — such as lenders, suppliers, or employees.

Examples of liabilities include:

- Accounts payable

- Bank loans

- Salaries payable

- Taxes payable

- Interest payable

- Bonds issued to investors

Liabilities can also be split into:

- Current Liabilities (due within one year, like short-term loans or accrued expenses)

- Long-Term Liabilities (due beyond one year, such as long-term debt or lease obligations)

Liabilities represent the claims of creditors over a business’s assets and must be repaid over time, usually with interest.

Shareholders’ Equity

Also called owner’s equity or net assets, shareholders’ equity is what’s left after liabilities are subtracted from assets. It represents the ownership interest of shareholders in the company.

Shareholders’ equity includes:

- Common stock

- Preferred stock

- Retained earnings

- Additional paid-in capital

- Treasury stock (if repurchased by the company, it reduces equity)

This section grows when the company earns profits (retained in the business) or raises capital by issuing stock. It shrinks when losses are incurred or dividends are paid.

Accounting Equation Formula and Calculation

As stated, the accounting equation is:

Assets = Liabilities + Shareholders’ Equity

This formula is always in balance, and it’s used in the preparation of a company’s balance sheet, one of the three core financial statements.

Example Calculation:

Let’s say a company has the following:

- Assets: $200,000

- Liabilities: $120,000

Then:

Equity = Assets – Liabilities = $200,000 – $120,000 = $80,000

So:

$200,000 (Assets) = $120,000 (Liabilities) + $80,000 (Equity)

The equation is balanced.

What Is the Purpose of the Double-Entry System?

The double-entry accounting system ensures that the accounting equation remains balanced after every financial transaction. In this system:

- Every transaction affects at least two accounts

- There’s always a debit and a credit side

- The total value of debits must always equal the total value of credits

This method helps in:

- Detecting and minimizing errors

- Creating accurate financial statements

- Ensuring transparency and accountability

For instance, when a company borrows $10,000 from a bank:

- Cash (Asset) increases by $10,000 → Debit

- Loan Payable (Liability) increases by $10,000 → Credit

This keeps the equation balanced:

Assets (+10,000) = Liabilities (+10,000) + Equity (no change)

Real-World Example of the Accounting Equation

Imagine a tech startup receives $500,000 from investors in exchange for common stock. The business then:

- Spends $100,000 on computers and office furniture (assets)

- Takes out a $50,000 bank loan (liability)

Here’s how the accounting equation would look:

- Assets:

Cash = $500,000 (investment)- $100,000 (equipment purchase)

- $50,000 (loan)

= $450,000

- Liabilities:

Loan = $50,000 - Shareholders’ Equity:

Investment = $500,000

So:

$450,000 (Assets) = $50,000 (Liabilities) + $400,000 (Equity)

Again, the equation remains in balance.

Limits of the Accounting Equation

While the accounting equation is a crucial tool in accounting, it does have some limitations:

- Doesn’t Reflect Market Value:

Assets and liabilities are recorded at historical cost, not current market value. The balance sheet may not reflect true worth. - No Detail on Profitability:

The equation shows financial position but not performance. Income and expenses aren’t part of this equation directly — they affect equity over time. - Ignores Intangibles:

Brand value, goodwill, and employee expertise may not be fully captured unless acquired through purchase. - Not Error-Proof:

Just because the equation balances doesn’t mean there are no mistakes. For example, incorrect account classification or omission may still occur.

Despite these limits, it’s still an indispensable tool for bookkeeping, auditing, and financial reporting.

FAQs about the Accounting Equation

1) What Are the 3 Elements of the Accounting Equation?

The three key elements are:

- Assets – What the business owns

- Liabilities – What the business owes

- Shareholders’ Equity – The owners’ claims on the business after liabilities

These elements must always stay in balance.

2) What Is an Asset in the Accounting Equation?

An asset is a resource owned or controlled by a business that provides future economic benefits. It includes physical items like cash, inventory, equipment, and intangible assets like trademarks or patents. Assets increase with inflows (revenue, capital) and decrease with outflows (expenses, depreciation).

3) What Is a Liability in the Accounting Equation?

A liability is an obligation that a company must settle in the future, typically by transferring assets or providing services. Examples include loans, accounts payable, and taxes owed. Liabilities represent claims of external parties on the business’s assets.

4) What Is Shareholders’ Equity in the Accounting Equation?

Shareholders’ equity is the residual interest in the assets of the business after deducting liabilities. It includes capital contributed by investors, retained earnings, and other components like treasury stock. It represents the true ownership value of the business.

If you’re learning accounting, mastering this equation is an essential first step. It’s the language behind every balance sheet and the reason why every debit must have a corresponding credit. Whether you’re a student, business owner, or aspiring CPA, knowing how the accounting equation works will unlock your ability to read and interpret financial statements confidently.